Arch Coal, Inc. Reports Third Quarter Results

Arch Coal, Inc. Reports Third Quarter Results

October 24, 2005 at 12:00 AM EDT

- Revenues increase to a record $654.7 million, up 24% vs. 3Q04

- Earnings per fully diluted share increase 63% to $0.26 per share (or $0.31 excluding special items)

- Income from operations rises 30% to $34.2 million

- Average realized price climbs 14% to $17.91 per ton

- Sales volume increases 8% to 35.2 million tons

- Adjusted EBITDA rises 29% to $92.0 million

October 24, 2005

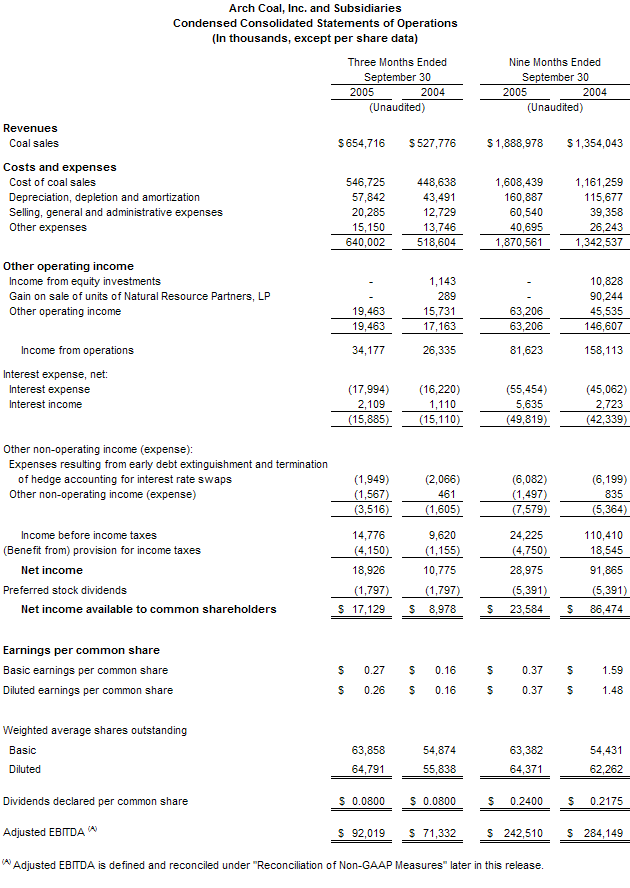

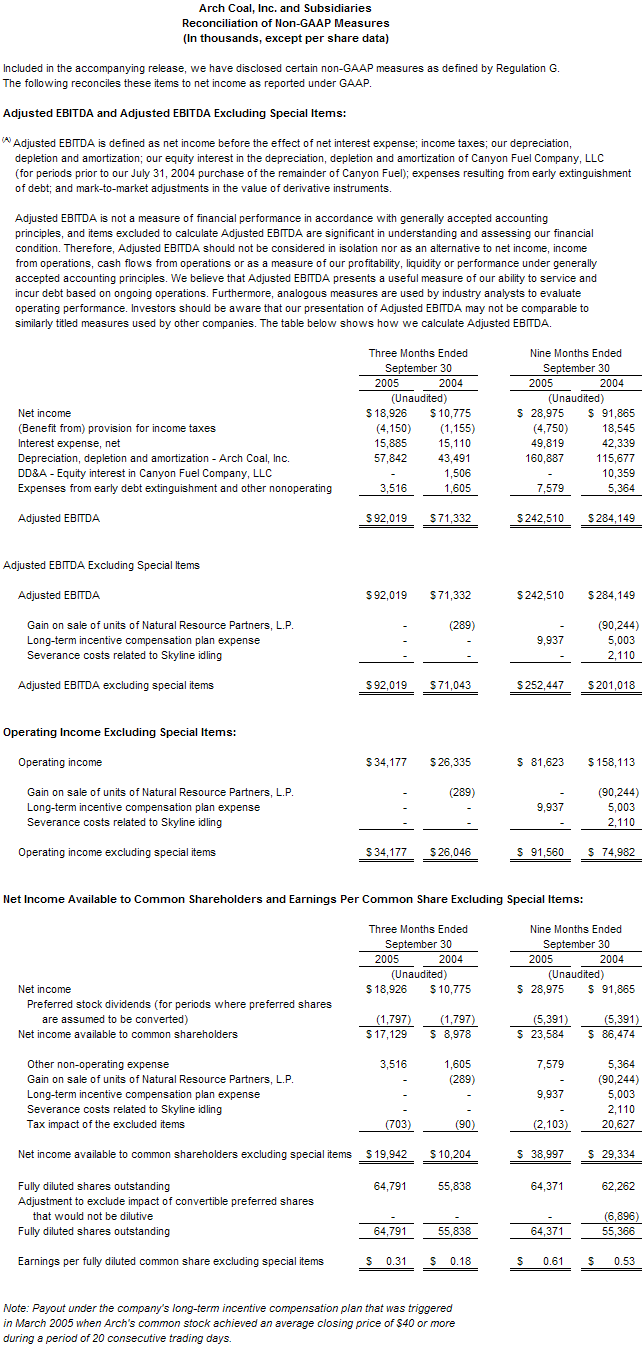

St. Louis - Arch Coal, Inc. (NYSE:ACI) reported today that it had income available to common shareholders of $17.1 million, or $0.26 per fully diluted share, for its third quarter ended September 30, 2005. Excluding special items, Arch had income available to common shareholders of $19.9 million, or $0.31 per fully diluted share. In the third quarter of 2004, Arch had income available to common shareholders of $10.2 million, or $0.18 per fully diluted share, excluding special items. (See the table that follows this release for a reconciliation to GAAP numbers.)

"Arch reported significantly stronger operating results during the third quarter, with substantial increases in revenues, operating income and earnings per share vs. the same period last year," said Steven F. Leer, Arch's president and chief executive officer. "Moreover, the outlook for U.S. coal markets continued to strengthen throughout the quarter. Coal stockpiles at U.S. power generating stations fell to their lowest levels in decades. The recent hurricanes in the Gulf of Mexico put further pressure on already stressed crude oil and natural gas markets. Prices for premium coal from the Powder River Basin of Wyoming climbed steadily throughout the period to levels approximately 200% higher than when the year began."

During the third quarter, revenues totaled $654.7 million, compared to $527.8 million during the same period last year. Sales volumes totaled 35.2 million tons, compared to 33.8 million tons during the same period last year as originally reported, or 34.8 million tons reflecting Canyon Fuel on a 100% basis. (Arch accounted for Canyon Fuel on the equity method prior to acquiring the remaining 35% interest in the company in July 2004.) Operating income for the third quarter totaled $34.2 million, compared to $26.3 million in the third quarter of 2004. Adjusted EBITDA totaled $92.0 million, compared to $71.0 million in last year's third quarter, excluding special items.

For the nine months ended September 30, 2005, income available to common shareholders totaled $39.0 million, or $0.61 per fully diluted share, excluding special items. (See the table that follows this release for a reconciliation to GAAP numbers.) That compares to $29.3 million, or $0.53 per fully diluted share, on a comparable basis for the same period of 2004. Revenues for the first nine months totaled $1,889.0 million and coal sales volumes totaled 106.9 million tons, vs. $1,354.0 million and 86.1 million tons in the comparable period of 2004, or 93.6 million tons reflecting Canyon Fuel on a 100% basis. Operating income for the first nine months of 2005 totaled $91.6 million excluding special items, compared to $75.0 million in the same period of 2004 on a comparable basis. Adjusted EBITDA totaled $252.4 million for the first nine months excluding special items, compared to $201.0 million for the same period of 2004 on a comparable basis.

Strengthening U.S. Coal Markets

It appears that coal consumption will outstrip coal production for the third straight year in 2005. Through the first nine months of 2005, power demand was up an estimated 4%, according to Edison Electric Institute, due principally to solid economic growth and warmer-than-normal summer weather. In comparison, coal production was up an estimated 1%, according to the Energy Information Administration. As a result, U.S. power plants ended September with an average of approximately 30 days of coal on hand, according to Arch estimates, roughly 25% lower than the five-year average for this time of year.

Coal demand remains exceptionally robust. While coal prices have moved up strongly in every producing basin, the cost of competing fuels has increased even more - and other fuel sources continue to be far more expensive options for generating electricity. Arch estimates that it is four to five times more expensive at present to generate electricity using natural gas than it is using coal. As a result, U.S. power generators have an enormous incentive to maximize utilization at their existing coal-fired power plants.

"Based on current production rates and continuing operating challenges in the eastern coalfields, it is conceivable that U.S. coal production could lag coal consumption once again in 2006," Leer said. Even after supply catches up with consumption, utilities will face a multi-year effort to rebuild coal stockpiles to more satisfactory levels, he added. "We believe that the foundation is in place for an extended period of attractive coal market dynamics and strong pricing."

In recent years, increasing utilization at existing coal-fired power plants has driven growth in coal demand. That trend is expected to continue, and will be augmented by several new demand drivers. First, U.S. power generators have announced plans to construct more than 70 gigawatts of new coal-fired capacity over the course of the next decade, representing a 25% increase over the current installed base. Several of these plants have already broken ground, while others are in advanced stages of development. In addition, coal's dramatic cost advantage vs. natural gas and crude oil - on an energy-equivalent basis - is spurring serious interest in technologies that would turn coal into commercial-quality natural gas or transportation fuels.

Arch has invested in select companies that are pursuing the development and deployment of such technologies, and plans to expand that portfolio over time. "We believe we can participate in the technology arena in a meaningful way by effectively leveraging our position as a leading U.S. coal producer," Leer said.

Regional Analysis and Other Data

Note: The above excludes 2.1 million tons of purchased coal in 3Q 04 in which Arch acted as the intermediary, creating a pass-through transaction. Per-ton costs have been adjusted to include the effects of amortization of values attributed to coal supply agreements in purchase accounting. Comparable amounts for all quarters beginning Q1 2003 can be found in the investor section of archcoal.com.

(1) For comparative purposes, Western Bituminous Region (WBIT) data reflect the results of Canyon Fuel Company at 100% in both periods, even though Arch accounted for Canyon Fuel on the equity method until acquiring the remaining 35% of the company on July 31, 2004.

(2) Per-ton realizations and costs as detailed above exclude certain transportation costs that are embedded in prices billed to customers. Powder River Basin transportation costs totaled $1.9 million in the third quarter of 2005 and $1.3 million in the third quarter of 2004. Central Appalachia transportation costs totaled $11.4 million in the third quarter of 2005 and $11.1 million in the third quarter of 2004. Western Bituminous transportation costs totaled $10.8 million in the third quarter of 2005 and $9.7 million in the third quarter of 2004.

(3) Per-ton costs detailed above exclude postretirement medical costs totaling $16.2 million in the third quarter of 2005 and $14.0 million in the third quarter of 2004.

Arch achieved significant increases in its average realized price per ton in each of its operating basins during the quarter. Compared to the same period of last year, average realizations were up 15% in the Powder River Basin, 28% in the Western Bituminous Region and 14% in Central Appalachia. "We expect this trend towards higher average realizations to continue and even accelerate as an increasing percentage of our existing contracts resets to market-based pricing," Leer said.

Higher per-ton costs at Arch's Powder River Basin operations reflected lower volumes associated with continuing rail challenges in the region, as well as higher royalties and production taxes associated with increased pricing realizations. Major maintenance and repair work on the joint line rail system in the Powder River Basin reduced Arch's third quarter shipments from the Black Thunder mine by two to three million tons.

In the Western Bituminous Region, favorable mining conditions contributed to a decline in operating costs compared to the same quarter last year, despite higher sales-sensitive costs.

"We continue to be very pleased with the performance of our western operations," said John W. Eaves, Arch's executive vice president and chief operating officer. "We are managing effectively the costs we can control, while offsetting many of the external cost pressures through process improvement initiatives. While cost pressures are likely to continue, we expect improving volumes at Black Thunder and our ongoing cost-control efforts to provide a counter-balance to that trend."

Operating costs have risen significantly in Central Appalachia during 2005, with most producers in the region facing pressure from higher diesel, explosives, steel and contract labor costs. "We are working aggressively to stabilize costs at our existing operations in Central Appalachia, while moving forward with the development of lower-cost reserves in the region," Eaves said.

Arch believes that its Mountain Laurel reserves in southern West Virginia represent one of the region's best remaining undeveloped reserve blocks. The company is developing a five-million-ton-per-year longwall mine at Mountain Laurel, which is scheduled to come on line in the second half of 2007, and plans to add a three-million-ton-per-year surface mine at the complex once all the necessary operating permits are in hand.

Arch's ongoing resource management efforts contributed $7.8 million on an after-tax basis to the company's quarterly results, principally on the sale of surface land.

Capital Spending and DD&A (in millions):

Note: Capital spending and DD&A data reflect Arch's 65% ownership interest in Canyon Fuel Company through July 31, 2004, and its 100% ownership position thereafter.

Sales Contract Agreements

Arch continued to take a balanced approach to its marketing efforts, layering in new sales contract agreements while maintaining a significant unpriced position for future periods. Since the beginning of 2005, Arch has reached agreements to ship approximately 30 million tons of coal annually in 2006, 2007 and 2008, at prices that range from 40% to 150% above the company's applicable average regional realized sales price in the third quarter of 2005.

Based on expected production over the next three years, Arch has unpriced volumes of 25 million to 35 million tons in 2006; 60 million to 70 million tons in 2007; and 90 million to 100 million tons in 2008.

Other Developments

During the quarter, Arch's southern Wyoming operations were honored with the nation's Director's Award for excellence in land reclamation from the U.S. Department of the Interior. It marked the second year in a row that an Arch subsidiary had received the nation's top reclamation honor. Earlier this year, Arch's Coal-Mac subsidiary claimed the Greenlands Award, West Virginia's top reclamation honor, marking the fourth straight year that an Arch subsidiary has been so recognized.

"Safe and responsible operating practices are at the very core of the Arch Coal culture," Eaves said. "We believe that long-term success in the coal industry depends on leadership in these crucial areas of performance. We are proud to say that our employees have embraced these values and are constantly striving to raise the bar still higher."

Looking Ahead

Over the course of the next three years, Arch believes that there are two principal drivers that should create significant new value for its shareholders: the ongoing expiration of legacy contracts and the company's portfolio of attractive internal growth opportunities.

Between now and 2008, the vast majority of Arch's existing contracts will expire and reset to market-based pricing. "If coal prices remain at current levels over that time frame, Arch expects to see significant increases in profits and cash flow," Leer said.

In addition, Arch believes it has some of the best organic growth opportunities in the regions in which it operates. These projects include:

- Completing the development of the Mountain Laurel complex in southern West Virginia, which is ultimately expected to produce approximately eight million tons of very high-quality coal per year.

- Completing the development of a three-million-ton-per-year longwall mine at a new reserve area adjacent to the former Skyline mine in the Western Bituminous Region.

- The eventual re-opening of the Coal Creek mine in the Powder River Basin of Wyoming.

Even after the restructuring of its Central Appalachian operations via the recently announced Magnum Coal transaction, Arch expects such internal growth projects to boost its wholly owned production by a net total of approximately 15 million tons annually by 2008. (In October 2005, Arch announced that it had signed a definitive agreement with affiliates of ArcLight Capital Partners, LLC to contribute certain of its Central Appalachian properties to a new company to be called Magnum Coal.)

While rail service remains a challenge, Arch is encouraged by the ongoing efforts of the western railroads to repair the existing rail infrastructure in the Powder River Basin, as well as recently announced plans to expand rail capacity substantially over the next few years. "We believe the western rail carriers share our view that Powder River Basin coal is poised to capture most new coal demand over the next five years, and that there is a great deal of work to be done by both the mines and the railroads in order to keep pace with such a robust demand environment," Leer said. The eastern railroads operated well during the quarter, Leer noted, despite challenges associated with Hurricane Katrina.

"America is becoming increasingly aware of the strategic nature of its coal resources," Leer said. "Our reliance on foreign sources of crude oil continues to rise, natural gas production in North America appears to have reached its peak, and the recent hurricanes in the Gulf have served to highlight the fragility of America's oil and gas infrastructure. New coal combustion technologies are exceptionally clean, and near zero-emissions coal plants are moving closer to reality. Coal liquefaction and gasification projects could significantly expand the marketplace for coal. With our modern mines, premier reserve base, and highly skilled workforce, Arch expects to capitalize fully on this exciting market environment."

A conference call concerning third quarter earnings will be webcast live today at 11 a.m. Eastern. The conference call can be accessed via the "investor" section of the Arch Coal Web site (www.archcoal.com).

Arch Coal is the nation's second largest coal producer, with subsidiary operations in West Virginia, Kentucky, Virginia, Wyoming, Colorado and Utah. Through these operations, Arch provides the fuel for approximately 7% of the electricity generated in the United States.

Forward-Looking Statements: Statements in this press release which are not statements of historical fact are forward-looking statements within the "safe harbor" provision of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are based on information currently available to, and expectations and assumptions deemed reasonable by, the company. Because these forward-looking statements are subject to various risks and uncertainties, actual results may differ materially from those projected in the statements. These expectations, assumptions and uncertainties include: the company's expectation of continued growth in the demand for electricity; belief that legislation and regulations relating to the Clean Air Act and the relatively higher costs of competing fuels will increase demand for its compliance and low-sulfur coal; expectation of continued improved market conditions for the price of coal; expectation that the company will continue to have adequate liquidity from its cash flow from operations, together with available borrowings under its credit facilities, to finance the company's working capital needs; a variety of operational, geologic, permitting, labor and weather related factors; and the other risks and uncertainties which are described from time to time in the company's reports filed with the Securities and Exchange Commission.