Arch Coal, Inc. Reports Second Quarter Results

EPS increases to $0.48 compared to $0.01 in prior-year period

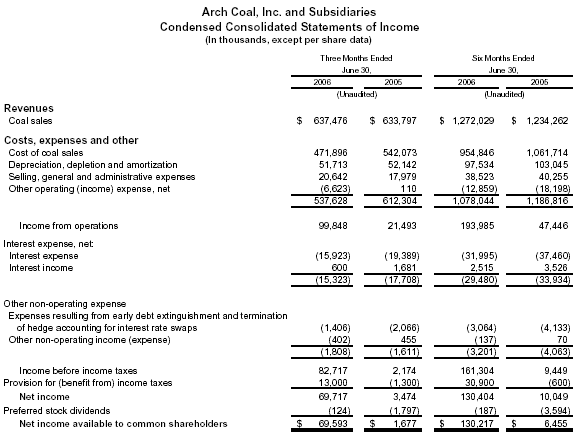

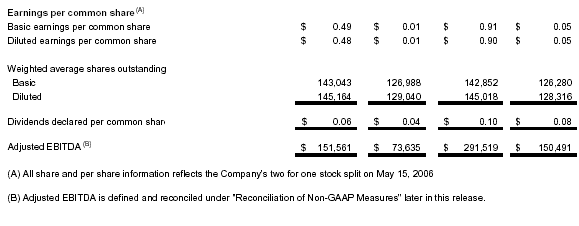

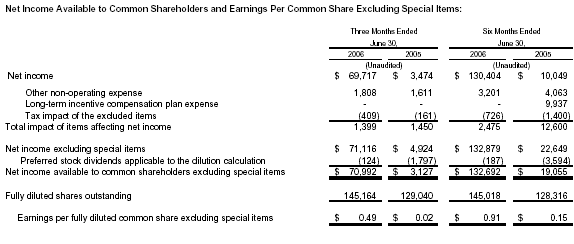

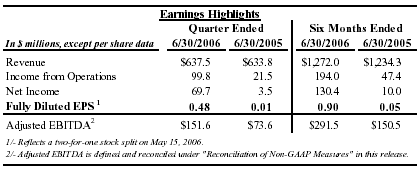

St. Louis (July 21, 2006) – Arch Coal, Inc. (NYSE: ACI) today reported second quarter 2006 consolidated net income of $69.7 million, or $0.48 per fully diluted share, compared with $3.5 million, or $0.01 per fully diluted share, in the prior-year period. All earnings per share figures reflect the impact of the company's two-for-one stock split on May 15, 2006. During the quarter, Arch also raised its dividend by 50 percent to $0.06 per share on a post-split basis.

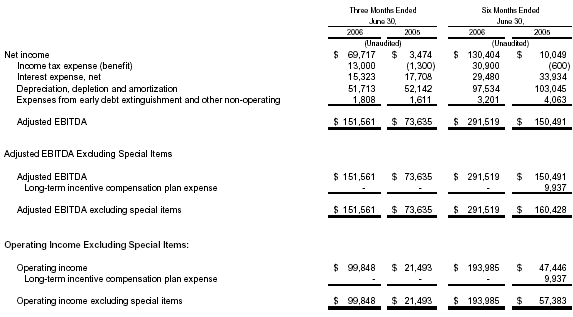

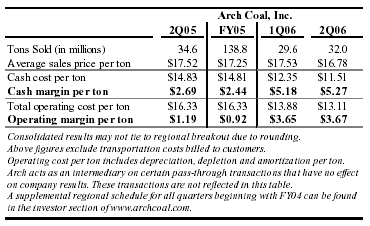

Arch achieved a more than fourfold increase in income from operations during the second quarter of 2006, reaching $99.8 million compared with $21.5 million from the prior-year period. Adjusted EBITDA more than doubled, rising to $151.6 million over the year-ago period, while revenues increased modestly despite the disposition of select Central Appalachian operations at the end of 2005.

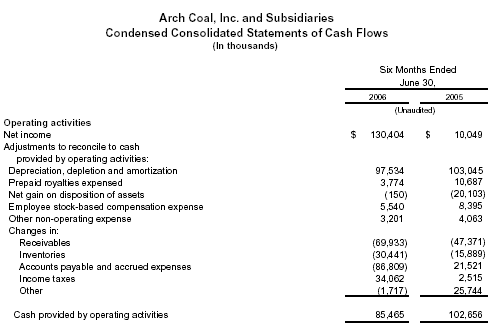

During the first half of 2006, Arch reported consolidated net income of $130.4 million, or $0.90 per fully diluted share, compared with $10.0 million, or $0.05 per fully diluted share, during the first half of 2005. Income from operations more than quadrupled to $194.0 million and adjusted EBITDA nearly doubled to $291.5 million over the prior-year period.

"Arch Coal achieved a strong operating performance in the second quarter of 2006, with substantial increases in EPS, operating income and EBITDA," said Steven F. Leer, Arch's chairman and chief executive officer. "Arch continued to deliver solid financial results despite rail bottlenecks and weaker near-term market conditions. At the same time, we began production at our Coal Creek surface mine in Wyoming and our Skyline longwall mine in Utah, managed costs very effectively and made good progress on our ongoing process improvement initiatives."

Arch Executes A Strong Operating Performance

"We are pleased with the company's operational performance during the second quarter and first half of 2006," said John W. Eaves, Arch's president and chief operating officer. "We look to build upon this strong performance in the second half of the year."

While consolidated volumes and price realization mix were impacted by the disposition of select Central Appalachian operations at the end of 2005, operating margin per ton increased substantially due to the roll-off of lower-priced sales contracts and the restructuring of Arch's Central Appalachian assets.

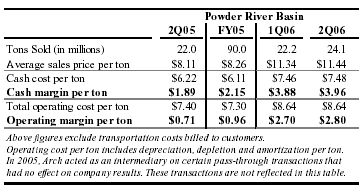

In the Powder River Basin, sales volume increased 2.1 million tons in the second quarter of 2006 compared with the second quarter of 2005, driven by improved rail service compared to the significant disruptions experienced last year. The restart of Coal Creek also contributed to the higher sales volume from the year-ago period. Average price realization rose by $3.33 per ton over the same time period resulting from the roll-off of lower-priced sales contracts. Operating margin per ton nearly quadrupled compared with the prior-year period.

When compared with the first quarter of 2006, sales volume rose by 1.9 millions tons and average price realization increased modestly. Of the 24.1 million tons shipped in the second quarter, approximately 600,000 tons related to Coal Creek. Average price realization and operating margin rose modestly over the same time period as gradually improving rail performance offset higher unit start-up costs at Coal Creek.

In the second half of 2006, Arch expects its shipments to accelerate in the PRB with the anticipated completion of additional rail infrastructure and the further ramp up of Coal Creek. Additionally, Arch expects the increasing volumes at Coal Creek to result in a modestly lower average price realization as well as a lower average unit cost during the year's second half.

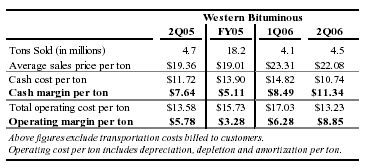

In the Western Bituminous Region, sales volume declined 200,000 tons in the second quarter of 2006 compared with the second quarter of 2005 as shipment timing and a longwall move impacted the quarter just ended. Average price realization rose by $2.72 per ton over the same time period resulting from the roll-off of lower-priced sales contracts. Operating margin per ton increased over 50% due to higher price realization as well as an insurance recovery of $10 million associated with the outage of the West Elk longwall mine in late 2005 and early 2006.

When compared with the first quarter of 2006, sales volume rose by more than 400,000 tons due to the resumption of operations at West Elk and the start up of Skyline. Of the 4.5 million tons shipped in the second quarter, approximately 200,000 tons related to Skyline. Average price realization declined over the same time period due principally to a less favorable contract mix. Operating margin expanded $2.57 per ton from the prior-quarter period due principally to improved productivity at the mines resulting from the restart of West Elk in March 2006. (Both the first and second quarter of 2006 benefited from separate insurance recoveries of $10 million related to West Elk.)

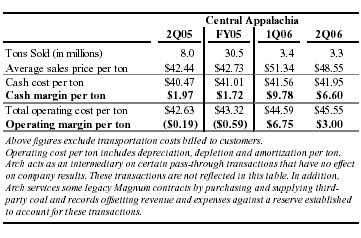

In Central Appalachia, volume comparisons between the second quarter of 2006 and the second quarter of 2005 were impacted by the divestiture of select operations in December 2005. Average price realization rose by $6.11 per ton over the prior-year period resulting from the roll-off of lower-priced sales contracts. Operating margin per ton improved dramatically over the same time period, from a negative $0.19 to $3.00 in the second quarter in 2006 resulting from the restructuring of Central Appalachian operations.

When compared with the first quarter of 2006, average price realization in Central Appalachia declined due to lower and delayed metallurgical coal sales as well as lower realizations on spot sales. Some of the delayed metallurgical coal sales are expected to occur in the second half of 2006. Operating cost per ton increased modestly during the same time period as a result of lower sales volume in the quarter.

Western Rail Performance Improves Modestly

While Arch has seen a modest increase in the number of daily trains servicing Black Thunder, additional throughput by the railroads will be needed to reach the mine's planned production rate. One such project to increase throughput is the construction of the triple track section of the joint line adjacent to Black Thunder. The additional track and supporting infrastructure is expected to be completed late in the third quarter.

"The completion of a third track south of Reno Junction – where Black Thunder's rail spur joins the main line – is expected to increase the overall fluidity of the rail system and should benefit Black Thunder in particular," said Eaves.

Arch Maintains Significant Unpriced Position

Given the weaker near-term pricing environment, most of Arch's sales contracting activity during the second quarter consisted of short-term deals associated with its uncommitted 2006 production volumes. Arch's 2007 and 2008 unpriced positions remain virtually unchanged from the first quarter of 2006.

Based on current expected production over the next three years, Arch has unpriced volumes of 7 million to 11 million tons in 2006; 55 million to 65 million tons in 2007; and 85 million to 95 million tons in 2008.

The company still has a significant percentage of its coal under sales contracts signed in earlier periods, when market conditions were weaker than the current environment. Within the next three years, the vast majority of these commitments will expire, and volumes are expected to be re-priced based on market conditions at the time.

"We continue to expect strong domestic and global demand growth for coal, coupled with supply pressures in the Appalachian basins, to exert a positive influence on coal pricing in coming years," said Leer. "The mild winter and spring have weakened near-term market conditions in 2006, but the energy needs of the U.S. and the rest of the world are growing dramatically. Arch believes that maintaining a significant unpriced position at this time is strategically advantageous."

Long-Term Fundamentals in Coal Markets Remain Strong Despite Near-Term Weakness

Arch believes that long-term fundamentals of the U.S. coal industry remain intact, despite weaker near-term conditions.

- A healthy U.S. economy will lead to increased electric generation demand, the majority of which will be supplied by coal. The U.S. economy is growing, with annualized gross domestic product up a strong 5.6% for the first quarter of 2006. Furthermore, the industrial production index, a measure of domestic manufacturing activity, reported annualized growth of 4.5% through June 2006.

- The cost of competing fuels continues to rise, creating a compelling economic incentive for utilities to maximize coal-fired utilization at existing power plants. The price of natural gas in the futures market for delivery this winter remains above $9 per million Btus, a far more expensive option for generating electricity than coal.

- Planned new coal-fueled capacity announcements in the U.S. have reached 93 gigawatts, equating to approximately 325 million tons of incremental coal demand and increasing coal's installed base by 30%, according to government and industry sources. At least 19 gigawatts – representing 67 million tons of new annual coal demand – are expected to come online by 2010.

- Worldwide coal markets are robust, fueled by increasing coal consumption in fast-growing economies such as China and India. In addition, tight supply conditions, driven by insufficient investment in the development of reserves, inadequate transportation infrastructure and labor challenges, continue to positively impact seaborne coal prices.

- Crude oil is currently trading above $70 per barrel. Furthermore, the geopolitical risk associated with the location of major world oil (and natural gas) reserves has continued to bring the public policy debate of domestic energy security to the forefront. As a result, the outlook for the advancement of Btu-conversion technologies, such as coal-to-gas and coal-to-liquids, remains favorable for the coal industry.

Furthermore, Arch believes that certain factors affecting some Central Appalachian coal producers may benefit the U.S. coal industry, and Arch in particular, in coming years. Beset by higher costs, permitting issues and a softer pricing environment, weaker Appalachian coal producers may struggle to keep up the current pace of production.

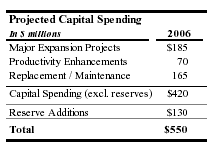

Arch's Capital Spending Program, Focused on Organic Growth, Is On Target for 2006

In 2006, Arch continues to target capital spending of $420 million, excluding reserve additions. Incremental production resulting from the completion of these projects is expected to total around 23 million tons per year by 2008.

"Arch is executing on its organic growth initiatives with the start-up of the Coal Creek mine in the Powder River Basin and Skyline's North Lease mine in the Western Bituminous Region, as well as the development of the Mountain Laurel complex in Central Appalachia," said Eaves. "Possessing superior geology, low capital costs, strategic location, or a combination of all three, these projects are expected to deliver an attractive return on our investment."

Arch Affirms Guidance For 2006

Arch affirmed its guidance for full year 2006, with earnings per share projected to be within the range of $1.87 to $2.12, on a post-split, fully diluted share basis, while adjusted EBITDA is expected to be in the $570 million to $610 million range. Total sales volume is expected to be between 135 million to 140 million tons, excluding pass-through tons of approximately 8 million associated with legacy Magnum contracts that Arch is currently servicing.

"We expect a strong second half performance," said Leer. "Furthermore, Arch remains sharply focused on delivering shareholder value via anticipated increases in price realizations, margins, earnings and cash flow in coming years, benefiting from contract roll-offs and strong operational execution."

Arch currently anticipates three longwall moves in the third quarter of 2006 as a result of shifting two moves from June to July. Additionally, ongoing railroad maintenance and construction activity, coupled with the timing of miners' vacations and associated mine maintenance, should impact operations in the upcoming quarter. "Consequently, we expect the third quarter to be our weakest operating period of the year while the fourth quarter is expected to be our strongest," said Leer.

"We believe that the long-term fundamentals of U.S. coal markets remain strong," said Leer. "Coal's economic advantage over natural gas in electric generation markets has led to a significant level of new coal-fueled capacity announcements, which is expected to translate into meaningful incremental coal demand by the end of the decade. Additionally, public interest in domestic energy independence and the price of oil is swinging momentum in favor of real investment in Btu-conversion technologies."

"Going forward, we expect our size, distinct asset portfolio and low-cost operations to enable us to deliver strong financial results, while positioning Arch to capitalize on the very promising long-term outlook for the U.S. coal industry," said Leer.

A conference call regarding Arch Coal's second quarter financial results will be webcast live today at 11 a.m. EDT. The conference call can be accessed via the "investor" section of the Arch Coal Web site (http://investor.archcoal.com).

Arch Coal is the nation's second largest coal producer, with subsidiary operations in Wyoming, Colorado, Utah, West Virginia, Kentucky and Virginia. Through these operations, Arch provides the fuel for approximately 6% of the electricity generated in the United States.

Forward-Looking Statements: This press release contains "forward-looking statements" – that is, statements related to future, not past, events. In this context, forward-looking statements often address our expected future business and financial performance, and often contain words such as "expects," "anticipates," "intends," "plans," "believes," "seeks," or "will." Forward-looking statements by their nature address matters that are, to different degrees, uncertain. For us, particular uncertainties arise from changes in the demand for our coal by the domestic electric generation industry; from legislation and regulations relating to the Clean Air Act and other environmental initiatives; from operational, geological, permit, labor and weather-related factors; from fluctuations in the amount of cash we generate from operations; from future integration of acquired businesses; and from numerous other matters of national, regional and global scale, including those of a political, economic, business, competitive or regulatory nature. These uncertainties may cause our actual future results to be materially different than those expressed in our forward-looking statements. We do not undertake to update our forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required by law. For a description of some of the risks and uncertainties that may affect our future results, you should see the risk factors described from time to time in the reports we file with the Securities and Exchange Commission.